Stop Home Scams: Knowing what to look for

COVID-19 has created a housing insecurity crisis. Families across the country are struggling with newfound uncertainty and increasing fragility surrounding their living situations. Unfortunately, scammers use crisis situations like these to prey on people’s fears and insecurities. That’s why it’s so important to pay attention to and learn more about housing scams.

Luckily, our friends at NeighborWorks America are partnering with the Wells Fargo Foundation, National Fair Housing Alliance and National Foundation for Credit Counseling to create a public education initiative aimed at helping consumers take action to protect themselves and their homes from scammers. They have already offered helpful tips to identify and avoid scams:

Do not pay anyone who is not your mortgage lender.

If someone contacts you and asks about home payment, do not pay them. The only entities that should be dealing with your mortgage payments are you, your lender and your certified housing counselor if you’re working with one. Additionally, if anyone gets in contact with you to tell you to stop paying your monthly mortgage payments, do not listen to them. Trying to get someone to halt their payments is a sure sign of a scam.

Do not give any personal or financial information to someone you do not know.

A great general rule is to not give any personal information to anyone who is not a licensed professional or personal friend, especially over the phone. That being said, if someone calls requesting information regarding your personal finances or housing situation, do not answer their questions until you can credibly verify who they are. If you cannot, there is no reason to move forward with any further conversation.

Do not listen to promises.

Someone might try to contact you and tell you that they can fix whatever housing insecurity you might be facing. For example, the person might promise to prevent your home being foreclosed on, or might promise to give you money for your next monthly payment. All payment plans should be arranged directly with your mortgage lender and your housing counselor – and neither will EVER promise you they can stop foreclosure or eviction. They will only provide the best options and counseling with the goal of preventing home loss. Promises of “free” money without certified counseling and expert intervention are a sure sign of a scam, as nobody can guarantee you will not be foreclosed upon or evicted. Also, if someone promises to provide a housing-related service for you, such as lawn care, do NOT pay them before the service has been completed, no matter how sincere their “promise” to get it done is.

Find out what your options are

One of the best ways that you can fight against scams is by becoming informed and arming yourself with knowledge as early in the process as possible. Talk to one of United Housing’s HUD-certified housing counselors, or any one of our team members. We want to help you find housing stability and give you real, practical ways to help you with whatever obstacles you may be facing. Regardless of moratorium deadlines, we can help you get on the path to foreclosure prevention now. The earlier you start the process, the better. Visit https://www.uhinc.org/education/foreclosure-counseling to get started with one of our counselors.

If you are suspicious that someone has tried to scam you or a neighbor, whether they were successful or not, please report the situation to the appropriate authorities such as the Federal Trade Commission (FTC) or the Consumer Financial Protection Bureau. For more resources on stopping scams, visit https://www.stophomescams.org/.

Foreclosure in Memphis: what you need to know

If you’re facing foreclosure in Memphis because of hardships caused by COVID-19, there is help out there for you. By connecting with United Housing, you’ve come to the right place.

No one expects you to know what to do on your own when you’re facing foreclosure. Our team of educated housing counselors can help you better understand the options you have that could help you keep your house. They will also walk you through the process – you do not have to go through this alone. You can start the housing counseling process by filling out this online form. If you’re facing foreclosure, we encourage you to sign up as soon as possible.

Before you start housing counseling, there are a few things you can do on your own. By taking these steps, you’re gathering information that will help your housing counselor and could help you keep your home.

To help you create a plan, our housing counselors need to know who owns your loan. If you’re not sure, you can use this free online tool to find out. Why is this important? Different lenders handle foreclosure support differently. Knowing who owns your loan will help us create the best repayment plan for your family.

2. Learn about CARES Act support and forbearance.

Government support can be confusing, especially when it comes to homeownership. Even if you read or watch the news and try to keep up with the most recent changes, it’s easy to misunderstand what help is available. This online tool from Freddie Mac explains important topics you should understand before you attend your counseling session: forbearance and CARES Act support. Read through this guide and click on the “+” icons to expand specific topics. Reading through this page a few times can help you better understand these topics and how they apply to your situation.

3. Prepare questions for your counselor.

You don’t have to come to your housing counseling session knowing everything about the CARES Act and forbearance. But reading about these topics ahead of time can help you prepare questions. As you read through the interactive online guide from Freddie Mac, write down questions for your housing counselor. They will be able to answer your questions and explain topics in more detail.

4. Continue to follow United Housing for more help.

United Housing is here to help. When you follow us on Facebook, you can learn about upcoming workshops or classes from United Housing and other trustworthy organizations in Memphis. These classes and workshops are a great way to learn more about housing, homeownership and specific topics like foreclosure.

If you live in Memphis and need help to keep your home, reach out to United Housing today. You can visit our website or call 901-272-1122.

How does debt factor into the homebuying process?

Finances are highly personal, and it can feel overwhelming when you’re trying to buy a home and you suddenly have to share a lot of personal financial information. You might even feel judged or embarrassed to share your debt information with a potential lender. The average American is about $38,000 in debt, so you are certainly not alone if you enter the homebuying process with outstanding debt. But it’s important to understand your personal financial information in relation to your debt and how that will impact your homebuying process.

How does debt impact my ability to buy a home?

Debt is one of the largest factors mortgage lenders consider when you apply for a home loan. Specifically, mortgage lenders will look at your debt-to-income ratio – or how much of your monthly income immediately goes toward paying down your existing debt. If you think about it, you consider your debt-to-income ratio every month when you make purchasing decisions. In your budget, you likely subtract your expenses (like debt repayment) from your income to determine how much money you can spend in a month. Your mortgage lender is doing this same process.

The specific debt-to-income ratio your mortgage lender is looking for will vary. But generally, most lenders look for a debt to income ratio below 43%. Of course, a lower debt-to-income ratio is favorable to lenders because it means you are more likely to be able to cover the cost of your mortgage on a monthly basis without overextending yourself financially.

Another way debt might impact your ability to buy a home is through your credit score. Your credit score is an easy way for financial institutions to see how reliable you are as a lender. Your credit score is built using a number of factors, but many of them are linked to debt. You can build your credit score by making your debt repayments on time every month, limiting outstanding debt on credit cards and reducing the number of debt accounts you have at one time.

Is all debt the same to my mortgage lender?

Most common types of debt are considered equal to mortgage lenders. Things like autopayments, student loans, personal loans and credit cards are all factored into your debt-to-income ratio. But, it’s important to talk with your lender, as some debts might be treated differently depending upon your mortgage options. For example some lenders subtract alimony payments from your monthly income but don’t include it in your debt-to-income ratio. This can sometimes make it easier for you to qualify for a loan.

There are a few things that you might consider debt that aren’t by your mortgage lender. Things like your monthly phone plan, gym memberships, or other subscription services are not counted as debt. It is still important to factor those costs into your monthly budget, though.

How can I use information about my personal debt to make a smart homebuying choice?

Understanding your personal financial situation, including your outstanding debt, is important to help you make the best homebuying decision for your family. When you work with one of United Housing’s homebuying counselors, they can help walk you through that process. Some families might need to work on paying off debt and raising their credit for a year before starting the homebuying process. Other families need to closely monitor their budget to determine how large of a mortgage payment they can comfortably afford. Regardless of your situation, our team of well-trained experts will help you understand your financial situation and will guide you toward the decision and home that is right for you.

Gentrification vs. Revitalization – What’s the difference?

When you move into a neighborhood, you want to see new businesses rise up on your block, neighbors renovating their houses, and general improvements happening around you. But, not all improvement is equal, and sometimes too much improvement can put you, the homeowner, in a difficult financial position. Today, we’re going to talk about gentrification, the dangers of this process, and a community-centered alternative.

What is gentrification?

As its defined by Webster’s New World College Dictionary, to gentrify means “to convert (a deteriorated or aging area in a city) into a more affluent middle-class neighborhood, as by remodeling dwellings, resulting in increased property values and in displacement of the poor.” Simply put, gentrification is the process of changing the texture and culture of a neighborhood and raising prices along the way to the point where original homeowners can no longer afford to live there.

If you think about the city you live in, you can likely think of examples of gentrified neighborhoods. From the outside, gentrification often looks appealing. Residents from outside of the community view it as “cleaning up” the city and adding amenities that “all” people can share. But in reality, gentrification pushes often long-standing residents out of their homes as property taxes, rental rates and home prices rise.

Why does gentrification happen?

There are a number of reasons why gentrification happens. Oftentimes, investors target “inexpensive” neighborhoods in close proximity to neighborhoods with more wealth. They take advantage of the lower barrier to entry that comes with purchasing foreclosed or unoccupied properties, and they quickly add new amenities to attract money from outside of the neighborhood. Once a few investors come in and find success, other investors come in and do the same thing to businesses and houses. It continues to escalate from there – often to the point where people are approaching homeowners or traditional businesses and asking them to sell their space to make way for “progress” in the neighborhood.

Why is gentrification harmful?

Healthy cities need neighborhoods with varied home sizes and prices. This helps the most people find stability and create generational wealth through homeownership. The greatest harm that gentrification poses to neighborhoods is the displacement of long-term residents living in “inexpensive” neighborhoods. As property values increase, so do taxes. Sometimes, homeowners are forced to move because they can no longer afford to live in the neighborhood. Simultaneously, as outside investors plant businesses in neighborhoods undergoing gentrification, patrons start filling the pockets of outside investors. This does not keep capital in the community in the way that supporting a locally owned business would. In addition to displacement and money leaving the community, gentrification can strip the cultural texture of a neighborhood. Local eateries, businesses, parks, art installations, and even architectural style are changed during the renovation process. The features that original residents love about the neighborhood can start to fade away as outside influences make changes.

What’s the alternative?

You can improve and strengthen neighborhoods without gentrification, and the key is supporting revitalization efforts within the community. Through programming, like the business development programming sponsored by JPMorgan Chase, neighborhood residents can receive funding and training to open businesses in the communities they call home. By supporting local business growth, you are adding amenities and resources, encouraging cultural maintenance while investing capital into your neighbors. Another example is the Binghampton Community Land Trust. This coalition of active residents oversee renovation projects in the neighborhood. They identify blighted properties and invest funds to turn these homes into viable, affordable options for future homeowners. The projects have financial restrictions that help maintain home values in the neighborhood.

United Housing works with financial institutions, the City, homeowners and other community development organizations to prevent gentrification and support community revitalization through strategic investments. We believe that this is one of the best ways to preserve communities, promote homeownership and strengthen our city.

Equity through Community Banking

Community banking

As you drive through your town, you’ve likely noticed community banks without even realizing you’re passing them. A community bank is exactly what it sounds like – a smaller, locally owned and operated bank that serves those in a particular area or community.

There are a few major differences between community banks when compared to regional and national banks. Community banks cannot serve customers out of state and instead focus on serving a specific set of customers in their area. For this reason, community bankers tend to understand the economic conditions of the area as well as the people who live there. This understanding makes community banks more likely to loan to borrowers in their community based on familiarity and family history rather than credit scores or traditional financial metrics. Additionally, community banks are small businesses themselves, making them more small business friendly. Community banks are a critical part of a healthy financial community because they are able to use traditional banking activities to pour back into their respective communities without some of the barriers that come with regional and national banks.

Banking and systemic discrimination

Most importantly, community banks are often located in underbanked communities in rural areas or inner cities. In urban, inner-city areas, community banks often serve a large Black population, which is significant as the Black community has been historically discriminated against financially, largely by regional and national banks. In an interview with NPR, Black bank owner Sidney King points out that many Black communities often feel big, national banks aren’t for them, as their parents and grandparents didn’t have banking relationships due to this systemic bias. Community banks that serve Black individuals are often also minority or Black-owned and can be vital to rebuilding trust between financial institutions and the Black community.

What now?

Unfortunately, race-based discrimination in banking still exists. Last year in Memphis, 13% of Black shoppers were denied a mortgage, while only 5% of white shoppers faced the same rejection, and predatory mortgage lenders are still more likely to target people of color.

United Housing has always worked to break down barriers that traditionally underserved Memphians face in the homeownership industry. Through loan programs like our new Build Bold Fund, we hope to raise money and forge partnerships with community banks to support individuals who cannot get approved for a loan through a regional or national bank. Another great way to combat financial inequity in your community is by supporting and investing in your local community bank. By opening a checking account or taking out a loan through a community bank, you are pouring your resources back into your neighborhood and the people who call it home.

Community banks give Memphians of all backgrounds the opportunity to be approved for loans and less likely to turn to potentially predatory lenders for financial help. To learn more about being approved for a loan, contact United Housing today at 901-272-1122.

Three things to do before you list your home

Preparing to list your home can be a time-consuming process. Many families spend weeks organizing closets, touching up paint and cleaning all the nooks and crannies to make sure their home is ready for potential buyers to visit. Preparing to list your home, especially if you have big plans to move, can be an exciting process! In all of that excitement, a few important steps might fall through the cracks. Here are three things to add to your to-do list that will help you get the most money out of your home as you prepare to sell:

1. Hold your own inspection to identify any issues you might need to fix.

When you purchased your home, you likely enlisted a home inspector to examine the house before you closed. Traditionally, buyers hire home inspectors to ensure the home they’re purchasing doesn’t have any outstanding issues or problems that should be considered in the sale process. It is common for buyers to request sellers to make repairs to problems as part of their contract. Unfortunately, many sellers enter the process without knowing these problems exist. When sellers have to make repairs or lower their selling price, they ultimately cut into the money they take home after they sell.

Before you list your home, hire an inspector to come out and thoroughly review your home. This inspector should be able to identify issues that you should repair before your home goes on the market, giving you time to make updates before you list. Even if you don’t choose to make the repairs recommended by the inspector, you will go into the selling process with a better understanding of what a potential buyer might ask you to repair or fund as part of the sale. This can help you determine a fair asking price and set your expectations for profit.

2. Research comparable home prices in your neighborhood.

A large part of the homebuying and selling process is setting personal expectations. You can save yourself a lot of heartache and struggle during the negotiating process if you base your asking price on research. In the months leading up to listing your home, track home prices in your neighborhood. You can do this online or using resources in the local newspaper. See how much money people are paying for homes comparable in size to your own within your zip code. Consider not only homes that have the same square footage as you, but also take into account how many bedrooms and bathrooms your home has compared to homes you’re watching. A house with more bedrooms or bathrooms than yours might sell for a higher price even if the square footage is comparable. If you use online sites like Zillow, Redfin or Trulia, you can also see the condition of homes in your neighborhood. Understanding how your home compares in terms of updates and renovations can give you a better understanding of your future asking price.

3. Enlist the help of a reliable Realtor.

A lot of sellers are tempted to list their homes themselves because of the commission fees that Realtors take after the sale. But partnering with a Realtor can save you a lot of time and money, so we always recommend working with an agent you trust. A Realtor can help you make decisions that will impact your sale – like the time you list and whether or not you should have an open house. When they walk through your home, they can identify your home’s best assets based on market trends and can tout those in your listing language. They often have access to professional photographers who will make your home look exceptional in online listings. Though you should do your research in step two, after walking through your home and surveying your neighborhood, your Realtor can help you set a realistic asking price. All of these factors will ultimately help you get the most money out of your home when you finally sell.

Affordable home maintenance for older homes. What resources are available to help you refurbish or maintain an older home?

The average home in Memphis is 46 years old, meaning many homeowners in our community live in houses that have been around longer than they have. Most people have great experiences in old homes, however, their rich history means they might be in need of a little more TLC. So, what options are available for you to do some home maintenance on your older home?

Simple touches

Don’t let outdated finishes or a bit of wallpaper discourage you from buying an older home! There are simple things you can do to refurbish your old home that only require a hardware store and a little dip into your budget. Things like adding fresh or new coats of paint, replacing door knobs or cabinet pulls, and investing in a new light fixture or two can make a home feel brand new. Some repairs you can do easily and inexpensively, such as filling holes left in a wall or using a little oil to fix a squeaky door. However, many older homes need work done that requires a professional, significant financial investment, or both. Luckily, there are several resources available to help you maintain your home.

MLGW weatherization and home repair programming

MLGW’s Share the Pennies is a community contribution program that allows homeowners to round up their bill payments and apply the money toward grants for low income tenants to make weatherization or energy efficiency repairs to their homes. This not only provides assistance to make necessary home repairs that old homes often need, but helps you to save money in the long run by cutting energy costs and lowering your utility bill.

Post Purchase support and Home Repair Loan options through UHI

Older homes can present serious challenges that you’ll want to address – they may need a new roof, lead-based paint abatement, new HVAC, foundational updates, and much more. Luckly, United Housing offers several resources that can help you with the process of refurbishing or maintaining an older home. Our Home Repair Loan program can help you upgrade your home for accessibility and security, and can be used for a variety of projects including plumbing, roofing, electrical and more. The loans range from $5,000 to $15,000 and have a low, fixed interest rate with affordable monthly payments over a repayment term of 10 years. You can click here to find out if you’re eligible for a home repair loan. Additionally, UHI offers Post-Purchase homeowner workshops that focus on teaching new homeowners how to successfully navigate homeownership by providing education on budgeting, credit, insurance and other financial responsibilities that come with owning and maintaining a home.

Old houses are charming, and are usually very well built and full of character – but you might find a few more needed renovations in them than you would in a newer home. However, don’t let that discourage you. Call United Housing at 901-272-1122 and start making plans as to how you could fix up your house. With the necessary support and resources, you can create a home for you and your family to enjoy for years to come.

How to talk with your children and family about eviction or foreclosure

Due to COVID-19, many families are finding themselves faced with the possibility of eviction or foreclosure. These things can be frightening as an adult, so it is especially scary for kids who might not even be exactly sure what these words mean – which is why you should talk openly about these issues with your children. These are struggles many people with and without children face, the best thing you can do is talk openly about it with your kids. Here’s how:

Be honest

It’s important to be honest when speaking with children about sensitive topics like eviction and foreclosure. Don’t hide anything from them, and be sure you answer all of the questions they might have. Of course, you do not have to tell them everything, but giving them some information will allow them to better navigate the situation and is better than leaving them in the dark.

Include them

Another way to extend your conversations with your kids about these topics is by keeping them updated and included in the process. Now, you don’t have to take your child with you to meet with a lawyer, however, it’s important that they know what could be coming next. Try to explain what steps you might be taking soon and how it could affect them. This will allow them to feel more at ease, as they’ll know what to expect, while also teaching them life skills that could come in handy in the future.

Provide reassurance

While this can be a difficult time, it’s important that as an adult, you try to have a handle on your own emotions during conversations with your child surrounding these topics. Kids will be scared and anxious, so you should be someone they can turn to with their questions and uncertainties. Be strong for them by acting as you normally would, providing them with the reassurance that although their housing situation might change, you will not.

Consider its impact on them

Above all, be cognizant of the individual changes your child might have to go through, and the significant impact it can have on their lives. It could be more than just moving homes, but potentially moving school districts and leaving a neighborhood of friends and familiar faces. It’s common for us to view kids as resilient, which they are, but we shouldn’t discount the profound impact change can have on their lives

It’s important that you remember that these things, although they might feel like it, are NOT the end of the road, and finding yourself with an eviction notice or with your home in danger of foreclosure, has nothing to do with what kind of parent you are, and how much you love your family. Homeownership is still possible, regardless of any setback. Call United Housing today, and we can help you get back on your feet.

How do adjusted mortgages play out?

If you contacted your mortgage provider about a forbearance and were approved, you might be wondering how repayment works. The good news is that you’re not expected or required to repay your missed mortgage payments in one lump sum. There are several common options you might be presented with – each with its own benefits and drawbacks. Here are several options you might receive and the facts about each:

1. Repay in one lump sum.

If you have the financial means to repay your mortgage in one lump sum, this is a great option to pursue. Of course, it requires a large lump sum of money up front. But, you do not accrue additional interest, and you can enjoy the relief that comes from paying off the debt. However, this is not an expectation, and you should not put yourself in a financial bind to pay off missed payments in one lump sum.

2. Pay more toward your mortgage each month for a period of time.

Your lender might allow you to increase your monthly payment for a period of time until the amount of your missed payment is satisfied. The benefit that comes with this option is that you do not extend the life of your loan, and therefore do not pay more in interest over time. However, this option might not be feasible if you are still experiencing financial hardship or have a restricted budget.

3. Add your missed payments to the back end of your loan.

Your lender could allow you to add missed payments to the end of your loan, extending the life of your mortgage by several months. If you cannot afford to make additional payments now, this is a great option. However, you will end up paying more over time for your loan as you will accrue additional interest. The additional expense over time could vary greatly depending upon the value of your home and the terms of your loan.

4. Adjust your loan payments entirely and extend the life of your loan.

If your financial circumstances have changed and your current mortgage payment is no longer feasible, your lender may allow you to adjust the terms of your loan in a way that lowers your monthly payment. This is a great option if you are looking for a way to keep your home and fear that you won’t be able to make payments if your monthly mortgage stays the same. However, adjusting the terms of your loan could impact your interest rate and will likely extend your mortgage, meaning you will pay more in the long run. But, a home is an investment, and this is a great option that will allow you to stay in your home long term.

5. Place missed payments into a junior lien, which must be repaid if you refinance or sell your home.

Some mortgage lenders will place a junior lien against your home for the total sum of your missed payments. This sounds more intimidating than it is – really, all it means is that when you sell your home or refinance your home, you have to pay back the loan before you can take a profit. So, if you’re going to sell your home for a $15,000 profit, and your lien is $3,000, then you’ll actually take home $12,000. This option cuts into future earnings but doesn’t impact the life of your loan or your interest rate.

It’s important to remember that each of the options above might not be presented to you. You’ll have to talk with your lender about your options to determine which is best for you. If you’re struggling to choose between repayment plans, talk with the housing counselors at United Housing by calling 901-272-1122.

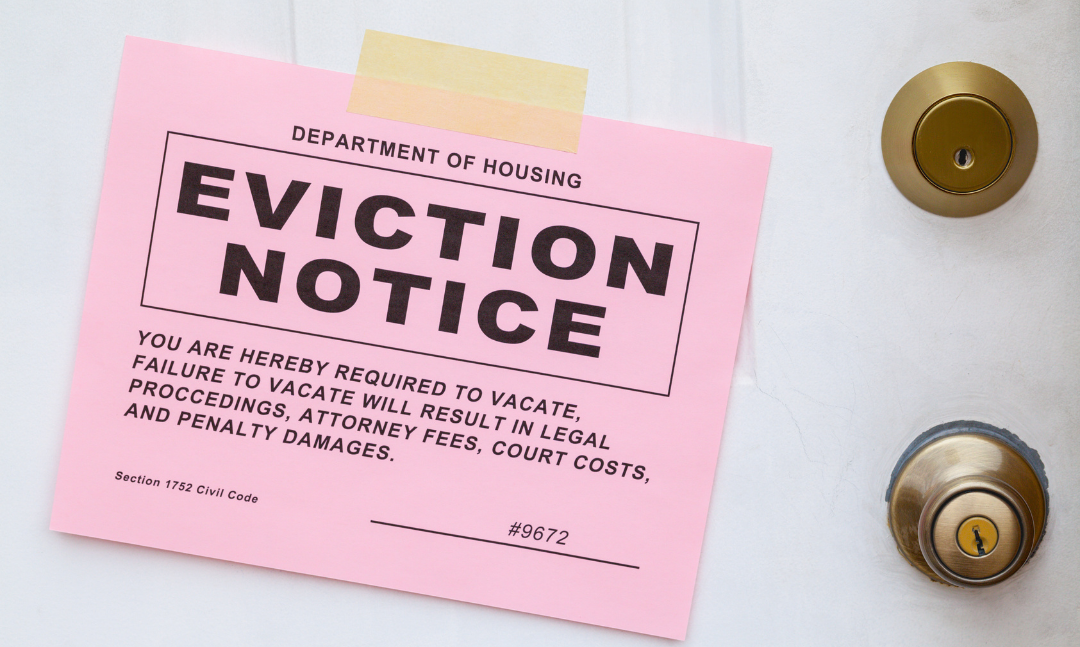

Eviction is not the end of the road

Our city is facing an eviction crisis – and you or a loved one might be trying to navigate the process. While local agencies, nonprofits, attorneys and community activists are working to keep people in their homes, it is likely that hundreds, if not thousands, of families will lose their homes over the next few months.

The eviction process can be disheartening, traumatic and confusing. To have the roof over your head taken away from you can lead you to a negative emotional state. But there is still hope – even if you’ve been evicted there are organizations like United Housing that want you to get back on your feet and guide you toward homeownership.

Is homeownership realistic if I’ve been evicted?

Yes. There is no situation where a person cannot start working toward homeownership. Some individuals work toward this goal more quickly than others, but the team at United Housing will support you for as long as it takes to get you into your new home. We can help you build your credit, which might be affected by your eviction if your late payments were turned over to a collection agency. Then, we’ll help you build a budget so you can save for homebuying expenses. We’ll educate you on the homebuying process and connect you with reputable loan officers. There is a path toward homeownership for everyone.

Why homeownership?

Owning your home creates a more stable environment, one where you’re in control. Homeowners don’t have to answer to landlords or leasing agents, and many feel empowered because they own the place where they live. In Memphis, many of our clients find that the mortgage they pay on a home they own is less than they paid in rent, making budgeting easier for many families while simultaneously providing more space and independence. Homeownership is also an investment in yourself. Every mortgage payment you make is an investment in the future profit you make when you go to sell your home.

What does this process look like?

It starts with asking for help. Our team of trained professionals are here to help assess your situation and provide support. From connecting you with immediate housing support to creating a credit improvement plan and helping you apply for loans you need, our HUD Housing Counselors and loan officers are here to support. What are you waiting for? Call UHI today at 901-272-1122.

Homeownership is for everyone – including young people

Homeownership is an intimidating process that many people think is too complicated or expensive for them to pursue. Historically, candidates for first-time homebuying were in their mid-20s through their early 30s. The generation that is currently within this age, millennials, carries $1 trillion in student loan debt, exponentially more than any previous generation. For some people, this debt fills the line in the budget previously allotted for housing.

Whether or not student loan debt is a factor, many young people assume that they could never afford to buy a house. Others believe they simply don’t need to buy a house. And while homeownership may seem out of reach, it is achievable and beneficial for most people with planning, budgeting and education. We’re debunking four homeownership myths to help you see how attainable and helpful homeownership can be for young people.

1. I have to have a 20% down payment to buy a house.

A down payment is the amount of money a homebuyer puts forward at the time of sale. While conventional mortgages require a 20% down payment to buy a house, there are other common mortgage loan types with more manageable down payment requirements. Federal Housing Administration and Veterans Affairs loans are great options for many young people and first-time homebuyers, and they require as little as 3.5% down. There are also down payment assistance programs offered by local and state governments for down payment assistance. Through these programs, qualified buyers can buy a home with 1.5% down. That makes the amount of money you have to save to start the process more affordable.

2. It’s cheaper to rent than it is to own.

One of the best things about purchasing a home is the control you have over what you spend. As you’re looking at houses, your mortgage lender can tell you the estimated cost you’ll pay per month for each house you’re considering. One thing that surprises UHI clients is that you can often finance a home so your mortgage payments are less than what you’re currently paying in rent! You can absolutely find a home that fits your desired monthly payment – below, at or above what you’re currently paying in rent.

3. I don’t have a partner, so I could never afford the payments.

Homeownership is not dependent upon your relationship status. Many young homeowners can afford to purchase a home and live on their own, but some people like the company of roommates. As the homeowner, you act as the landlord to your roommates, collecting rent to help cover your mortgage payments.

Depending upon the size of your house, the number of roommates you have and your monthly mortgage note, you might be able to free up some of your personal budget to save for unexpected repairs, home renovations or other expenses.

4. I’m taking on a lot of risk buying a house – I don’t want to be stuck here forever.

Any major investment assumes some risk, and a house is no exception. However, property and a home are some of the most stable investments a person can make. You’re never guaranteed equity, but most homes appreciate in value over time. So, if you’re planning on staying in your current city for the next few years, you’re likely to make a little bit of money if you buy a home. Buying a home is an investment in yourself and your future – renting is an investment in someone else’s property.

Best ways to beat the summer heat

While summer brings a lot of fun, it also brings dangerously high temperatures. Here are a few tips to remember as you work to keep your house and yourself cool this summer:

Stay hydrated

The number one, and perhaps most important tip on our list is staying hydrated. Our bodies already need at least eight glasses of water a day, but we need even more water when we spend half of the day sweating! Drink plenty of water each day, and even more so when exercising or spending any time outside.

Treat yourself – don’t overheat yourself

While drinking water is always important, there are a few more fun ways to avoid overheating this summer. Enjoy your favorite cold dessert – popsicles, ice cream, you name it! If you’re able, visit a swimming pool to cool down. You could even invest in an inexpensive “baby pool” to inflate in your backyard, which is fun for the whole family to splash around in.

Keep the heat out

It’s easy to forget that heat can still enter your home without a door or window being open. The sheer sunlight alone can heat up your house! If you haven’t already, consider investing in curtains to cover your windows. Not only does it block sunrays, but it adds a nice touch to your living space. As you work to keep the heat out, be cognizant of the heat you create inside your home. Using the oven and the dishwasher both can heat up your home significantly, meaning heat-free recipes and manual dish washing might be a few things you should implement this summer.

Keep the air in

Allow cool air to constantly flow through your home without increasing your air conditioning bill too much. Utilize your ceiling fans throughout the day, and consider purchasing a few box fans to place in different areas of your home during the summer months.

This summer, don’t forget to be responsible, stay cool and have fun!

Ways to make your rental house feel like home

If you just moved into a new home, congratulations! Moving into a new space can be exciting, and making your new surroundings feel like home is probably one of your top priorities.

If you’re renting, then there are probably rules you have to follow. You may not be allowed to paint, hang things on the walls using nails or screws, or change out hardware. But there are still things you can do to make your space feel like your own! Here are a few recommendations we have for renters:

● Invest in mess-free hanging supplies. If you’re not allowed to drill or drive nails into walls, there are products you can use to hang things up! Products like Command™ Hooks are inexpensive and can be used to hang artwork, photos or other homey touches on your walls. Stores like Walmart, Target and Kroger will have several options to choose from! The best part – when you’re planning to move out, taking down your art is as easy as pulling a tab! The adhesive won’t pull off paint and can be removed in seconds.

● Consider buying a rug. Adding a rug or floor covering to a room can make it feel more full and inviting. Rugs are a great option if you don’t have enough furniture to fill a space, as they can give structure to a room and make it feel more full. Even if most of your rental unit is carpeted, you can still layer rugs on top of carpet to add new colors and textures to the room. Though rugs can get expensive, you can often find affordable options at stores like Ikea or HomeGoods. You can also try second-hand and thrift stores for great used options.

● Use what you have to decorate! You don’t have to purchase table runners or expensive decorative items to make your house feel more like a home. See how you can use items you already have to make your open spaces feel more filled. Keeping place settings of dishes on the dining room table can make your table feel ready for company. Adding books to your coffee table can add an interesting focal point for guests. Empty out and wash old candle glasses to create new storage canisters for bathroom supplies like cotton balls or swabs. Get creative with what you already have!

Important housing terms defined

Important housing terms defined

If you’ve experienced financial hardships in light of COVID-19, you’re not alone. Millions of Americans have filed for unemployment and others have been furloughed or had their hours significantly reduced. As we’ve shared before, we’re in the beginning stages of understanding what effects COVID-19 will have on housing, but we know that many of you needed to miss payments because of financial hardship.

We want to make sure you’re in the best place possible to navigate the repayment process. There are a number of factors to consider, and there are terms associated that can be confusing or unclear. Here are a few terms you should know as you start to build your repayment plan:

● Compounding interest may still accrue depending upon your debts. If additional payments are added on to the back end of your loan, your interest may compound and extend beyond your original payment plan. Talk with your lender about your interest rate and how deferment or forbearance might impact how much interest you pay on the life of your loan.

● Deferment is simply the process of pushing something back or moving it to a later time. If your bills or loans are deferred, like many individuals’ student loans are now, this means that they will be due at a later time. Check with your lender to learn what your repayment plan will look like.

● Forgiveness when it’s associated with a loan means that you are not expected to make repayments. This is rare for things like mortgages, utilities or rent payments. You may have heard this term in conversations about COVID-19 relief loans for businesses. Always check with your lender before you assume a debt is forgiven.

● Forbearance is an immediate relief program where one’s debts payments are no longer due on a regular basis. Forbearances usually have terms that you’ll know up front (usually listed as a number of days) and after the terms have expired you’ll be expected to resume payments. If your loan is in forbearance, you need to talk with your lender about the repayment process.

● Hardship is any circumstance that has made it difficult for you to make loan payments. Many deferment and forbearance programs require proof of hardship before you can miss payments. Hardship examples could include a termination letter, proof of reduced hours, or other documentation that demonstrates a loss in income related to COVID-19.

We know that this can be a complicated process to navigate. If you need help understanding your loan standing and determining a repayment plan, United Housing can help.

Three home projects you can do with your children

Staying in can cause even the best of us to go a little stir-crazy, especially when you have kids in the house who are even more bored than you. No matter the reason for your home stay, it’s important that you find activities to keep your mind moving. Why not do a fun, fixer-upper project and let your children help? It’ll cross something off of your list and keep them busy! Here are a few ideas:

Garden

Grab a few seeds and see what you can do! Gardening is a great activity that builds fine motor skills, teaches responsibility and is fun for the whole family. Planting some pretty flowers in your front yard increases your curb appeal, and can lift the spirits of your neighbors. Planting a vegetable garden is also a great idea – in a few months you’ll have fresh and healthy foods right at the tip of your green thumb! Not ready for a full garden yet? Purchase a few house plants and enlist your kids to help take care of them. Indoor plants are a great decorative piece that will spruce up your home and you’ll have extra sets of hands when it comes to daily watering!

Make a birdhouse

What better to go with your new garden than a birdhouse? With a little bit of wood and a pretty paint color, you have all you need to make one. A bird house is an adorable addition to your porch or yard and something you can always keep. For a little extra fun, use an old bottle and buy some seeds to create a bird feeder! Once your birdhouse is complete, you can watch from the window to see what types of birds make your birdhouse their home! This is a great activity to teach your children about nature and animals.

Paint something

Is there a room that desperately needs a fresh coat of paint? How about a wooden chair that would make your lawn look a lot brighter if it were painted yellow? Grab an inexpensive bucket of paint from your local hardware store, or maybe an old paint can stored in your shed, and get to painting! This is an activity that’s more fun the more people you get involved. There’s nothing like the sense of accomplishment you feel once you’ve completed painting something. If painting sounds fun to you and your children but you don’t have any pressing paint needs at the moment, get creative! Paint the inside of a small closet or maybe a bathroom cabinet, something that won’t drastically change your home’s appearance but will be fun nonetheless!

Show your kids that home improvement can be fun! Who knows, you may have a future builder, architect or designer on your hands.

Three apps to help you save money!

At United Housing, we’re all about using tools to help your money go further. We encourage all of our clients to budget and save so they can achieve their homeownership dreams.

We live in a digital world where there are many FREE tools that can help you save money! Here are three safe and reliable options:

Honey – Honey is an online app that helps you find coupon codes for the websites you use to buy essential supplies online! If you were already planning on making an online purchase, Honey can help you find the best deals and additional savings you might not have known about otherwise. It’s free, and really easy to use!

Mint – One of the best ways to save money is to realize how much money you spend. Mint helps users categorize their spending and set budgeting goals. It’s almost like a game for your wallet! Using Mint will help you understand where your money goes each month, and can help you save up for big purchases – like a house, a present or a vacation!

Ibotta – Why not get paid for the supplies you buy? Ibotta is an app that pays you back for the products you buy. Before you make a needed purchase, browse the Ibotta app to see if there is a cashback deal for a product you need. The catch is this, though – don’t buy things you don’t need just because you can get some money back! Ibotta really helps you save by paying you back for products you need.

What are you waiting for?! Start saving today!

What you should know about your credit score

There are still a lot of unknowns about the mid- and long-term impacts of the coronavirus on the financial well-being of Americans. Typically, missing or skipping payments on rent, utilities or other loans has a negative impact on your credit score. But with many financial institutions allowing missed payments, does that mean they will extend grace in relation to your credit standing? Not necessarily.

While we don’t know for sure how the coronavirus will affect your credit score, there are a few things you can do to put your best foot forward:

Learn what your current credit score is. Understanding your current credit score will help you track how it changes in the coming months. Without your current score as a baseline, it can be hard to tell if the score is changing over time. If you need help finding out what your credit score is, call United Housing at 901-272-1122.

Pay what you can. Continuing to make your regular payments is the best way to avoid a hit to your credit score. At the same time, try not to run a high balance on your credit cards. We understand that times are challenging, and making all of your payments may not be possible. Prioritize your family’s immediate needs, like food and shelter, first.

Keep detailed notes of any payments you skip. If you skip a payment of any kind, keep tidy notes so you can track progress toward paying them back. If you understand what you missed and how much you owe, you can work toward paying off your debt in a timely fashion. Repaying debts quickly will help prevent a major decline in your credit score.

Stay in continued communication with your lenders. We can’t say for sure what your personal repayment plans will look like. Talking with your lender about their repayment options will help you create a plan to repay your debt. You can prioritize based on deadlines and debt amounts to decrease your debt as quickly as possible. Again, if you carry debt for a shorter amount of time, your credit will be affected less.

If you have questions about managing your credit score, working with reliable lenders or building your credit, call us at 901-272-1122. We’ll be happy to help you and your family through these processes.

Three gardening projects you can tackle while at home

Don’t have a green thumb? No worries! Gardening doesn’t have to be expensive or difficult, and it can make a dramatic difference to your home’s curb appeal. Here are three small things you can do to spruce up your flower beds while you’re spending time at home:

1. Start by pulling weeds.

While this doesn’t sound like the most fun job, it is something you can get the whole family involved in! Create a game to see who can pull the most weeds out of your flower bet in 15 minutes. Then the winner gets to choose what is for dinner that night! You’ll be shocked how great your flower beds look in a matter of minutes.

2. Add mulch to your flower beds.

Mulch is an inexpensive and easy way to take your landscaping from boring to beautiful! There are a variety of colors and styles, and many of them are readily available at your local hardware store. All you need to do is call ahead and make a purchase, then swing by and pick up your mulch. If you’re not sure about how much to buy, talk with your local expert on the phone – they’ll help you determine how many bags to buy. Then, all you have to do is take your mulch and spread it!

3. Line flower beds with stones or bricks.

Does grass creep into your flower beds? You can create a clean line by adding stone pavers or bricks! While some options can be expensive, there are many inexpensive options you can choose from, especially if you want to line a small space. Order these pavers from your local hardware store, and then start lining! You can make it fun for your whole family by challenging the kids to design and color how they want the flower beds to look!

Interest Rates vs. Mortgage Rates

The economic market is in a state of uncertainty as financial institutions are trying to predict the outcome of the COVID-19 pandemic. There are a number of factors coming into play – from unemployment filings to gross domestic product – that paint a larger picture of the economic impact of the coronavirus.

One thing you’ve likely heard on the news or read online is that interest rates are falling. In an effort to stimulate the economy, sometimes the federal reserve will lower the interest rate to entice people to spend, which ultimately provides an economic boost. This means that interest rates on bank loans, car loans and other loan projects might be lower now than they were a few weeks or months ago.

It’s important to know that interest rates are not the same as mortgage rates. Mortgage rates are controlled by a number of different factors, and tend to rise in high-risk times. Because the economic future is uncertain, mortgage rates are rising. This means that mortgage rates are now higher than they were a few months ago. If you have a mortgage and your rate is locked, the change in mortgage rates does not affect your home loan.

Mortgage rates are ultimately out of a homebuyer’s control. While you want to get the lowest rate that you can, it should be noted that now is still a good time to buy a home if you’re in a strong financial situation. United Housing can help you prepare to make a home purchase through online and remote Homebuyer Education courses.

Three home projects you can take on!

As we’re all spending more time at home, there are things that you can do around the house to make your situation more comfortable and to improve the value of your home! These simple, inexpensive projects are great things to take on while staying at home.

1. Replace the hardware on your cabinets.

Is the hardware on your kitchen or bathroom cabinets outdated? You can easily replace those fixtures to add a fresh look to your space! There are many online retailers and hardware stores that have stylish options available for online purchase and home delivery. Make sure you’re ordering the appropriate size, and we recommend you purchase a few extra in case you need to replace a knob in the future – you never know when that style will go out of stock! This is an inexpensive change you can easily make on your own.

2. Create a statement wall!

Want to take a room you love up a notch? Consider creating a statement wall! A statement wall is simply one wall in a room that you cover with stylish wallpaper or different color of paint. Wallpaper is on-trend right now, and you can purchase inexpensive and nonpermanent peel-and-stick wallpaper from online retailers. Or, you can order a bucket of paint from your local hardware store and pick it up easily. It’s amazing what a fun pattern or a pop of color can add to your space.

3. Invest in outdoor lights.

Love to spend time outdoors? Adding outdoor lighting is a great way to liven up an outdoor patio, carport or deck. Retailers like Walmart and Target have outdoor lighting options at various price points that will fit within your family’s budget. Once you add outdoor lighting, your family can enjoy evening meals or time outdoors while still practicing social distancing!